|

THEMATICS| Fintech in Singapore

By GROW with Singlife Contributor : Farhan Ahmad Mumtaz Key Findings

Key Findings #1

Singapore is a top fintech jurisdiction globally, punching above its GDP weight in terms of its footprint. Its sound yet market-friendly regulatory framework makes it one of the most innovative established fintech centers globally.

Key Findings #2

Five funds offer exposure to the fintech theme; Nikko AM Shenton Thrift Fund, LionGlobal Singapore Dividend Equity Fund, LionGlobal Singapore-Malaysia Fund, Eastspring Singapore Asean Equity Fund and abrdn Singapore Equity Fund.

Overview & findings Singapore’s stable political environment, robust infrastructure, and pro-business policies make it a leading Asian fintech hub, with over 2,100 MAS-regulated firms as of 2024.

Supported by sound regulation, innovation-friendly policies, and a vibrant digital ecosystem, the sector thrives in areas like payments, wealth management, and digital banking, bolstered by strong venture capital funding and SGX access.

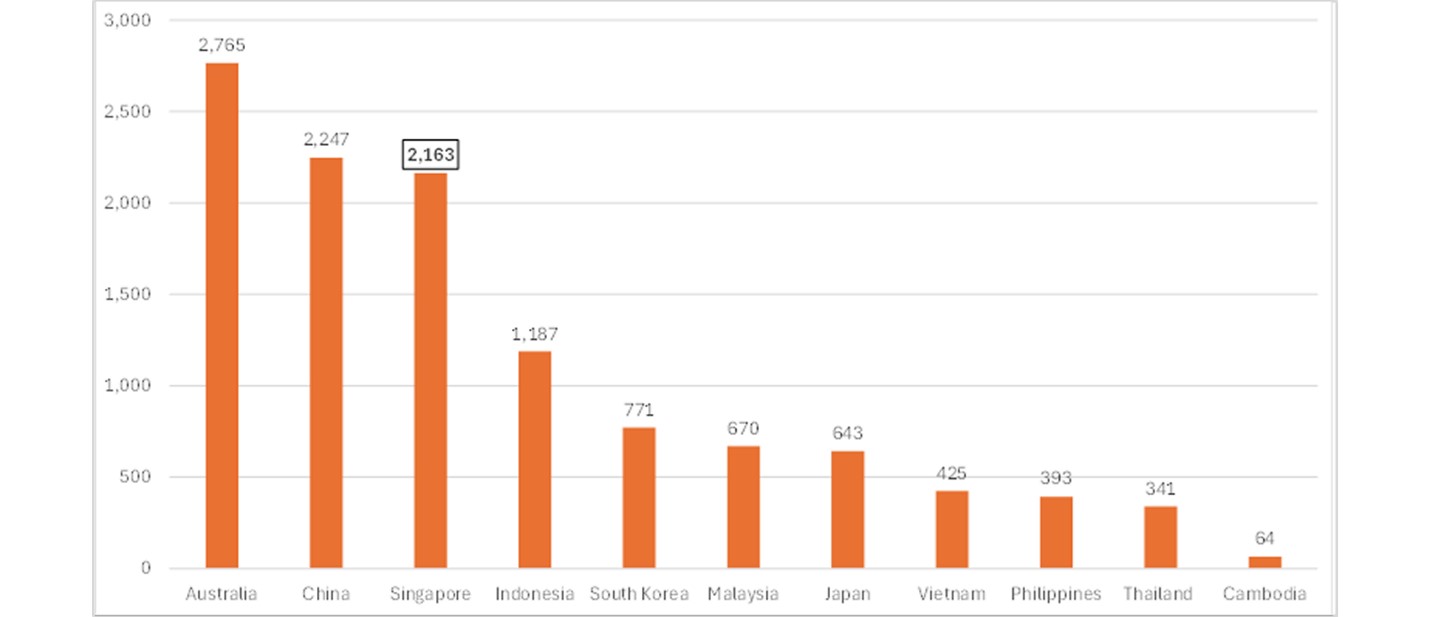

Singapore’s stable political environment, robust infrastructure, and pro-business policies are important contributory factors to its position as a leading Asian fintech hub. Solid economic foundations combine with a well-entrenched digital ecosphere and regulatory clarity with innovation-friendly policies for the fintech space. Singapore has over 2,100 fintech firms operating as of 2024 (see Figure 1), according to data from Tracxn.com, all of which are regulated by the Monetary Authority of Singapore (MAS).

The fintech ecosystem encompasses companies in payments, wealth management, Insurtech, regtech and digital banking supported by the sound regulatory infrastructure that MAS provides; this constructive environment has over the last few years seen major developments in the ecosystem including e-payments innovations (project Nexus), the establishment of a regulatory sandbox, the API exchange, the Singapore Financial Data Exchange and the Global Finance and Technology Network. It is also an established jurisdiction for venture capital and private equity funding of fintechs, supported by its low tax regime, with access to a domestic capital market (SGX) for potential investor exits.

Among the ten fintech companies we identify and discuss in this report, we highlight three stocks that have strong fintech attributes and also attractive from a market valuation perspective; these are UOB Kay Hian, Hong Leong Finance and United Overseas Insurance. Credit Bureau Asia is also an interesting stock and, although it does not qualify as a value stock, it generates premium returns that are trending higher.

Risks to the fintech sector’s further development and to companies’ fundamental prospects include;

MACROECONOMIC OVERVIEW

Combined with political stability, Singapore has solid economic foundations, a market-friendly regulatory framework with the added advantage of a tech-savvy population.

Chart 1:Singapore, top 3 SEA economy based on the number of active fintechs (August 2024 data)

Source: Tracxn

Singapore, as a growth market for fintechs, also provides a regional gateway into ASEAN markets, leveraging cross-border opportunities. The fintech ecosystem, supported by MAS, provides a culture of innovation and to some degree collaboration. SGX offers capital market access, and potential investor exits for successful fintechs in the form of domestic IPOs.

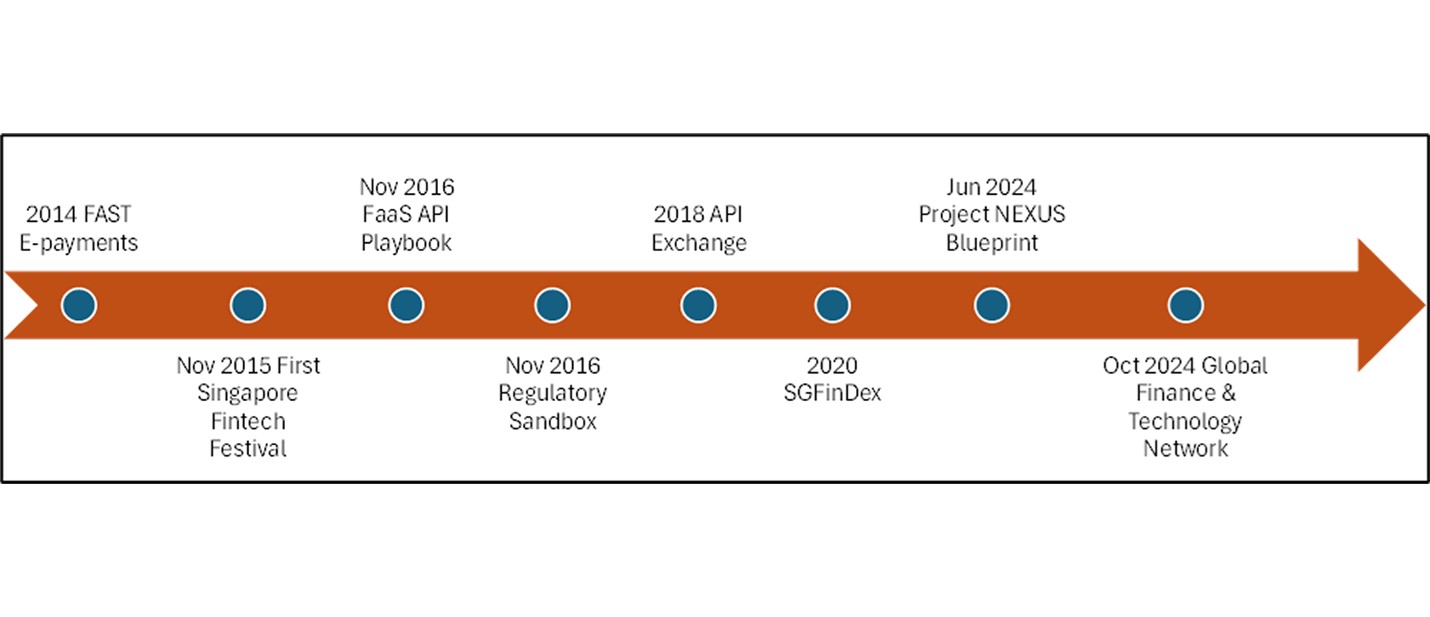

The Singaporean government, through MAS, has embraced market-driven regulation on fintechs; the regulatory timeline, involving much co-operation with the banking sector, Big Tech and other financials, has been marked by the chronological steps in the chart and bullets below;

KEY REGULATORY DEVELOPMENTS IN THE SINGAPORE FINTECH SECTOR

E-Payments Singapore has one of the leading E-Payments systems in Asia. Since the introduction of the FAST electronic funds transfer service in 2014, E-Payments innovation has developed at a fast pace with the addition of innovations such as UPOS (2016), PayNow (2017), NETS & EZ-Link (2017) and Singapore QR (SGQR) Code (2018); see the Singapore E-Payments journey in this timeline infographic.

The Finance-as-a-Service API Playbook In 2016, The Association of Banks in Singapore, in consultation with the MAS, published the Finance-as-a-Service API Playbook, providing comprehensive guidelines on API governance, implementation, use cases, and over 400 recommended APIs for banks (MAS API media release). This playbook contains information on common and useful APIs, technical and information security standards, and industry-relevant corporate data policy and governance, marking the beginning of the fintech regime in Singapore.

Fintech Regulatory Sandbox MAS launched the Sandbox in November 2016, supporting fintech experimentation; it relaxes regulatory requirements to enable live testing of innovative financial products and services within a controlled environment. This approach fosters innovation while ensuring consumer protection and financial stability. The framework was enhanced with the Sandbox Express in 2019 and the Sandbox Plus in 2021 (MAS Sandbox webpage).

The API Exchange (APIX) In 2018, MAS, in collaboration with the International Finance Corporation and the Association of Southeast Asian Nations (ASEAN) Bankers’ Association, launched the API Exchange, the world’s first cross-border, open-architecture platform (APIX media release). The exchange is a collaborative platform for fintechs and financial institutions to innovate and develop/test new products using open APIs. These APIs are tracked in the Financial Industry API Register run by MAS to provide a directory of open APIs offered by financial institutions domestically.

Singapore Financial Data Exchange (SGFinDex) This was implemented by MAS in 2020, enabling individuals to aggregate their financial data across banks and government agencies (SGFInDex media release). Most recently, the launch of the Singapore Trade Data Exchange (SGTraDex), a digital utility that connects supply chain partners through a common data infrastructure leveraging APIs, showcases Singapore’s continued efforts in propelling open finance specifically and fintech generally. While not mandatory, MAS has provided a robust framework and infrastructure to facilitate its open banking/finance adoption.

Project Nexus (e-payments) The blueprint for the project’s phase three was completed on June 30, 2024, with this multilateral initiative (BIS, MAS and other regional central banks) aiming to enable retail cross-border payments by interlinking domestic fast payment systems of member countries, including Singapore, Malaysia, Thailand, the Philippines, and India. The platform is expected to go live by 2025..

Global Finance & Technology Network (GFTN) Established in October 2024, GFTN is a non-profit organization led by former Monetary Authority of Singapore (MAS) Managing Director Ravi Menon. It aims to drive global fintech collaboration and innovation by offering advisory services to governments and organizations, connecting them with multilateral agencies and private sector partners, and investing in fintech and climate technology startups with social impact.

Singapore FinTech Festival (SFF) An annual event organized by MAS, SFF is considered one of the leading fintech trade shows globally; its ninth edition in November 2024 attracted 65,000 participants. The festival brings together various fintech communities worldwide, fostering collaboration and showcasing the latest innovations in the sector.

Chart 2: TIMELINE OF KEY REGULATORY AND ASSOCIATED DEVELOPMENTS IN SINGAPORE

Source: MAS

FINTECH SUB-THEMES: TRENDS AND DRIVERS

High smartphone penetration (97%) and a relatively young, tech-savvy population serves to support broad fintech adoption, with a backdrop of healthy GDP growth of approximately 4% in 2024.

Singapore offers some unique companies that are well positioned to take advantage of the fintech theme.

Digital Wealth Management/Wealth-tech

The prospects for wealth-tech in Singapore are positive given the city-state's status as a global financial hub, supportive regulatory environment, and growing demand for digital financial solutions. With increasing affluence in the region and a tech-savvy population, digital wealth management platforms, including robo-advisors and AI-driven tools, including personalized financial planning, are gaining traction.

Singapore's regulatory framework, backed by initiatives from MAS, fosters innovation while ensuring consumer protection. Emerging trends like ESG-focused investments, the integration of AI and big data, and hybrid advisory models present significant opportunities for growth, including increased adoption in the underserved segment for mass-affluent individuals.

Like other fintechs, Singapore is a leading jurisdiction that prioritises access to funding for wealth-techs whilst operating in a market-friendly regulatory climate. More importantly, Singapore’s cross-border wealth management connectivity is on the rise, due to its position as a key offshore wealth management hub in the region, driving increasing investment inflows. In terms of its domestic asset pool, its high pension penetration rate at 94% of GDP, comparable to that of its smartphone penetration, adds to Singapore’s potential for growth in the wealth-tech space.

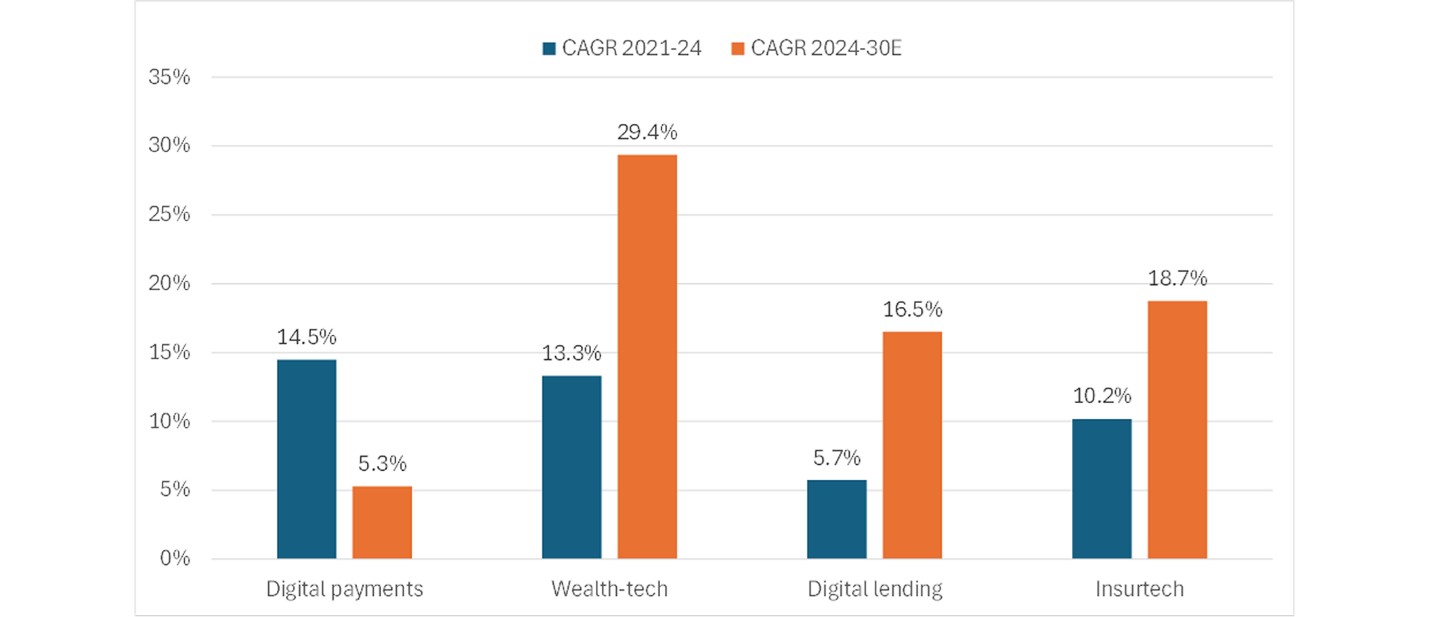

Wealth-tech AuM has increased in Singapore, its 2021-24 CAGR was over 13%; according to the e-Conomy SEA 2024 report, the 2024-30 CAGR is forecast to accelerate to 29% (see Figure 3). This expected fast growth rate is driven by digitally enhanced investment solutions, in terms of both B2B as well as B2C, and they include Robo-advisory that can also support IFAs in their servicing of retail clients.

Chart 3:Singapore Fintech sub-categories: wealth-tech and Insurtech are forecast to deliver premium growth

Source: e-Conomy SEA 2024 report

Digital Banking

Digital Banking and Credit has high growth potential: Singapore’s digital lending 2021-24 CAGR was close to 6%; according to the e-Conomy SEA 2024 report, the 2024-30 CAGR is forecast to accelerate to over 16% (see Figure 4). We estimate that digital credit penetration, as a share of total credit outstanding, stood at 1.5% in 4Q24; this implies that there is substantial potential for growth.

Since 2020, MAS granted four digital banking licenses two of these being Digital Full Bank (DFB) licenses and the other two being Digital Wholesale Bank (DWB) licenses, to act as a catalyst for innovation in banking and to enhance financial inclusion.

The DFBs are GXS Bank (backed by Grab Holding and Singtel) and MariBank, subsidiary of Sea Limited; the DWBs are ANEXT Bank, backed by Ant Financial and focused on SMEs, and Green Link Digital Bank, backed by Greenland Financial Holdings Group Co. Ltd, Linklogis Hong Kong Ltd, and Beijing Co-operative Equity Investment Fund Management Co. Ltd. In addition, Trust Bank was launched in September 2022 by Standard Chartered Bank and NTUC FairPrice without having to go through the typical application process for a digital banking license; Standard Chartered was already designated as Singapore's first Significantly Rooted Foreign Bank (SRFB) entity in 2020.

Digital Payments

MAS plays a pivotal role in fostering innovation through frameworks like the Singapore Payments Roadmap and regulatory sandboxes. The growing popularity of real-time payment systems like PayNow further enhances consumer and business adoption. The competitive landscape is vibrant, featuring traditional banks, fintech firms, and global tech giants offering a range of payment solutions, from mobile wallets and QR code payments to cross-border digital transfers so competition in intensifying especially from incumbent commercial banks as well as big techs.

The adoption of PayNow and SGQR have been two key developments that have streamlined digital payments for consumers and businesses alike. Recent introduction of SGQR+ enhances QR payment interoperability. In December 2024, the MAS and the Association of Banks in Singapore (ABS) announced plans to launch new Electronic Deferred Payment (EDP) solutions by mid-2025. These solutions aim to facilitate the transition from traditional cheque-based payments (focused initially on the corporate sector) to electronic methods, enhancing efficiency and reducing processing times.

Digital Payments to rise further: Transactions via e-wallets increased by 35% YoY in 2023. According to MAS statistics, cash withdrawals accounted for 29% of total payments in 2023, versus 31% in 2022. The 2021-24 CAGR of gross transaction value (GTV) of all digital payments in Singapore was 14.5%, the CAGR is expected to slow to 2030 and yet remain above 5% (see Figure 4), according to the e-Conomy SEA 2024 report. EDP and EDP+ should be a further catalyst for the growth in the share of digital payments.

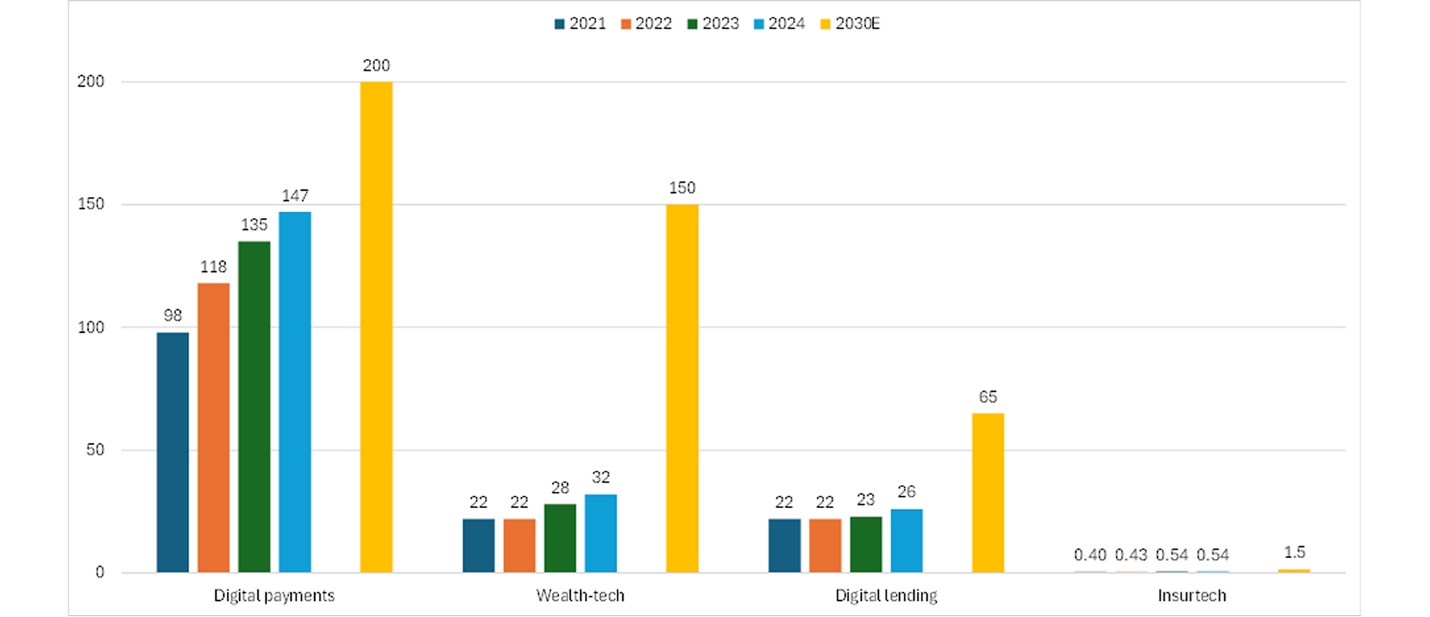

Chart 4: Digital payments and wealth-tech are the biggest categories by value

Source: e-Conomy SEA 2024 report

Insurtech

The outlook for insurtech in Singapore benefits from the country's status as a global insurance hub, a tech-savvy population, and a government committed to drive financial innovation. Insurtech firms are transforming the industry with AI and big data, enabling personalized policies, seamless claims processing, and improved customer experiences. MAS fosters innovation through initiatives like regulatory sandboxes and grants, creating an environment conducive to growth.

The competitive landscape features a mix of agile startups and established insurers adopting digital solutions or forming partnerships with insurtech firms to stay ahead; this all indicates a highly competitive landscape. Key trends include the rise of embedded insurance, parametric insurance, and the use of blockchain for transparency.

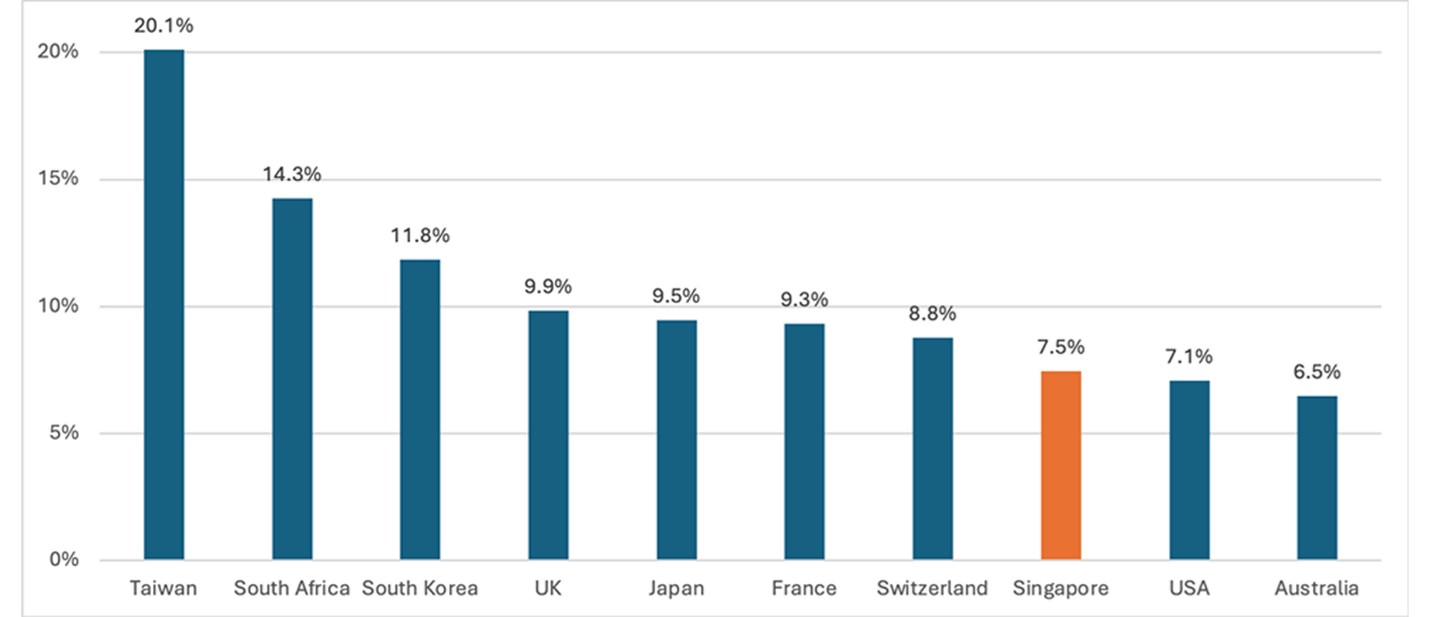

Singapore is in the top ten countries in the world in terms of insurance penetration, at over 7% of its GDP (see figure 5). The Insurtech market is forecast to grow fast, from a low level, with a 2025-2030 CAGR of close to 10% according to analysis by Mordor Intelligence. In January 2024, the MAS implemented a new regulatory framework targeting the nation's largest insurers, designated as Domestic Systemically Important Insurers (D-SIIs). This framework subjects D-SIIs to enhanced regulatory standards and closer supervision to maintain financial stability. In effect, this should serve to increase competition, resulting in a lower regulatory burden which should provide support for the growth of smaller insurers and new entrants into the Insurtech space.

This is another area of fintech that is expected to register an acceleration in its future growth Based on data from the e-Conomy SEA 2024 report, insurtech’s 2021-24 CAGR was over 10% and the 2024-30 CAGR is forecast to accelerate to close to 19% (see Figure 4); we see organic growth and the substitution of traditional insurance servicing for digital channels as key drivers.

Chart 5: Top ten nations in terms of insurance penetration (% of GDP)

Source: NationMaster website

Digital Credit

Digital lending in Singapore is underpinned by the country's advanced financial infrastructure, a highly digitalized economy including a solid fintech ecosystem, and a supportive regulatory framework. As businesses and consumers increasingly embrace digital platforms, fintech lenders are leveraging AI and big data to offer faster, more accessible, and personalized loan services. Initiatives from MAS, such as regulatory sandboxes, encourage innovation while ensuring market stability and consumer protection. The demand for digital lending is further bolstered by the rise of small and medium-sized enterprises (SMEs) seeking alternative financing options and the adoption of buy-now-pay-later (BNPL) solutions among consumers.

Software for Fintechs and Credit Bureau Services

As financial institutions and businesses increasingly prioritize automation, data analytics, and cybersecurity, demand for digital software solutions in areas like payments, wealth management, lending, and regulatory compliance is on the increase. As financial institutions and businesses prioritize risk management and creditworthiness evaluation, demand for advanced credit bureau services is growing. The competitive landscape features established players offering comprehensive credit reporting and scoring solutions, while newer entrants and fintech collaborations introduce innovative analytics financing further fuels the need for reliable credit data.

Stocks listed on Singapore Stock Exchange that offer exposure to Fintech Theme

SGX: U10 UOB-KAY HIAN HOLDINGS

UOB Kay Hian, a top Asian brokerage, leverages fintech innovations like robo-advisory services, digital investment platforms, and the UTRADE wealth management platform. It partners with firms like Goldhorse to enhance structured products and taps into UOB Group’s strengths to cross-sell. The firm covers fund management, unit trusts, derivatives, and corporate finance, with regional offices in key Asian cities. It boasts the highest market cap, best ROE, and lowest PE among its peers.

SGX: TCU CREDIT BUREAU ASIA

CBA is a leading provider of credit and risk information solutions in Southeast Asia, serving clients across Singapore, Malaysia, Cambodia, and Myanmar. It offers comprehensive consumer and commercial credit data, helping financial institutions make informed, timely decisions. CBA’s services include credit reports, risk assessments, credit scores, monitoring, data analytics, and customized solutions, enhancing clients’ risk management and decision-making processes.

SGX: S41 HONG LEONG FINANCE

HLF, Singapore's largest finance company and a top digital credit pick, integrates fintech to enhance services and customer experience. In 2022, it launched HLF FASTPAY, a multi-currency e-wallet with a virtual prepaid Mastercard for digital payments. HLF also leverages AI from its affiliate, Hong Leong Bank Malaysia. Its core activities include deposits, hire purchase, leasing, mortgages, secured loans, with expanded services in insurance underwriting, distribution, and FX

SGX: S35 SINGFINANCE

SingFinance is digitalizing its operations to enhance customer service and reduce costs, with initiatives like a digitally enabled core banking system, mobile app, web portals, and digital payments via SWIFT, FAST, and MEPS. It also offers online housing loan applications and multi-token mobile security. As a licensed finance company, it accepts deposits and provides loans, including property, construction, equipment, motor vehicle, and shipping loans, along with safe deposit boxes and financial guarantees.

SGX: TVV OXPAY FINANCIAL

OxPay, a high-risk micro-cap in payments, leverages advanced technologies to offer a unified API supporting over 150 currencies, streamlining payment processes, and enabling scalability. It provides BNPL options for flexible consumer payments and partners with GLDB to offer merchants easier financing, boosting retention. Focused on merchant payment and digital commerce services, OxPay delivers O2O solutions with integrated platforms for retail, transport, and F&B sectors. It operates in Singapore, Malaysia, Indonesia, and Thailand, aiming for regional growth.

SGX: I49 IFS CAPITAL

IFS Capital integrates fintech solutions to support businesses across Southeast Asia, including Malaysia, Indonesia, and Thailand. It offers a digital loan marketplace with Myinfo integration, providing access to 45+ lenders and streamlined applications. IFS also launched a supply chain finance platform to enhance liquidity for businesses and invested in Payd, an Earned Wage Access platform in Singapore and Malaysia. Its services include working capital loans, leasing, credit insurance, structured finance, and cross-border loans.

Fund Feature The following funds provide exposure to Fintech theme and can be found on the dollarDEX Fund Center

NIKKO AM SHENTON THRIFT FUND

The investment objective of the Fund is to maximize medium to long term capital appreciation by investing primarily in stocks listed on the Singapore Exchange Securities Trading Limited ("SGX-ST"). The fund’s weighting in Singapore is 94%, with financials making up close to 52% of the fund allocation. A differentiating factor from the other three funds is that it has a significant holding in SGX (5.3%), both a fintech in its own right and an exit option for Singaporean fintechs that IPO. Since inception (August 1987), the fund has delivered an annualized return of 6.0%. The fund size is SGD 414.3m.

BGF FINTECH FUND

The Fund is a global, industry diversified, all-cap strategy that seeks opportunities arising from technological disruption within the finance industry, with a focus on maximizing total return. With consumer behavior changing to increasingly favor innovative digital financial solutions over traditional methods, Fintech is making a significant impact across the whole financial ecosystem, and is poised to be a powerful force over the long term. The fund is managed by 2 Portfolio Managers holding a combined 30+ years of investment experience in the Financials sector and supported by 25+ FinTech, Financial and Technology analysts worldwide. The Fund’s high conviction portfolio of ~30-50 stocks is selected through a rigorous stress testing process, with an emphasis on identifying companies with idiosyncratic characteristics and notable re-rating catalysts and avoiding weak businesses and those exposed to potential regulatory hurdles.

FIDELITY FUND – GLOBAL FINANCIAL SERVICES FUND

The portfolio manager looks to invest in quality businesses at the right valuation. The investment approach combines bottom-up stock picking with top-down country and sector analysis. The manager identifies investment opportunities by leveraging Fidelity’s in-house research, company management meetings and varied investment themes. The focus is on strong businesses as well as companies with improving fundamentals that potentially translate into higher return on equity. The manager then assesses valuations to determine whether these are factored into the stock’s price and identify long-term winners. Thorough assessment and monitoring of ESG risks & impact of ESG factors on fundamentals and sentiment is carried out. Top-down macroeconomic considerations play an important role as the prospects for banks and other financials companies are tied to the economy. The objective of the fund aims to achieve capital growth over the long term. Its five largest holdings are JP Morgan, Berthshire Hathaway, Visa Inc, Wells Fargo and Mastercard Inc. Since the performance (strategy) commencement date (16th October 2013), the fund has delivered an annualized return of 7.8%. The fund size is USD1,436m.

GS GLOBAL FUTURE GENERATIONS EQUITY PORTFOLIO

The fund is designed for investors seeking exposure to a thematic and concentrated global portfolio that invests in companies that benefit from the consumption patterns of younger generations. Potentially higher returns may be generated but also increased levels of risk than from a more diversified global equity portfolio.Its five largest holdings are Apple Inc, NVIDIA, Amazon.com, Alphabet Inc and TSMC. Since inception (October 2018), the fund has delivered a total return of 101.6%. The fund size is USD 1,549m.

ABRDN SINGAPORE EQUITY FUND

The fund aims to generate capital growth by investing in Singapore equities. Indirect exposure to fintechs is achieved via its heavy weighting in Singapore financials (c 55% of exposure). Since inception (December 1997), the fund has delivered an annualized return of 7.9%. The fund size is SGD 900m.

DISCLAIMERS & CONFIDENTIALITY NOTICE IMPORTANT DISCLAIMERS This document is prepared by Navigator Investment Services Limited (UEN No.: 200103470W) ("Navigator") and is distributed for information only. It is not and does not constitute an offer, recommendation, or solicitation to enter into any transaction, to buy or sell any investment product, or to adopt any investment strategy in relation to any investment product. This document does not take into account the specific investment objectives, investment strategies, financial situation and needs of any particular person (including the intended recipient). You should not rely on any contents of this document as financial advice or recommendation to invest. Past performance is not indicative of future performance and no representation or warranty is made regarding future performance. All information and opinions expressed in this document were obtained from sources believed to be reliable and in good faith, but no representation or warranty, express or implied, is made as to its accuracy or completeness or any verification on such information and opinions has been performed. All information and opinions herein are current as at the date of this document, and subject to change without notice. To the extent permitted by law, Navigator specifically disclaims all warranties (express or implied) regarding the accuracy, completeness, or usefulness of this document and the information within and Navigator assumes no liability with respect to the consequences of relying on this document and the information within for any purpose. Navigator accepts no liability for any loss or damage arising directly or indirectly (including special, incidental or consequential loss or damage) from the use of this document. All investments are subject to risks including market fluctuation, risk, and possible loss of principal. Some investments may not be offered to citizens of certain countries such as United States. This document has not been reviewed by the Monetary Authority of Singapore (MAS). In line with MAS Fair Dealing Outcomes, we at Navigator are committed to Treating Customers Fairly CONFIDENTIALITY NOTICE This document is confidential and may contain information that is privileged. The sending of this document to any person other than the intended recipient is not a waiver of the privilege or confidentiality that attaches to it. If you are not the intended recipient, please destroy all copies of this document and do not copy, distribute or disclose this document or its contents and notify the sender immediately.

|

This website is meant for viewing only. To place order please go to www.dollardex.com