|

How Will Emerging Asia Fare in 2023? Q1 2023 Quarterly Insights by Manu Bhaskaran, CEO of Centennial Advisors

In summary, we see four big themes shaping Asia’s trajectory:

1. Global monetary tightening is peaking, but sticky inflation means higher rates for longer. The US and Eurozone central banks have shown a continued hawkish tilt, even in the wake of the SVB collapse and Credit Suisse takeover. Clearly central banks believe that the financial stresses we have experienced recently can be managed. Thus, expect continued but measured rate hikes across the US, Europe, and Asia, as inflation remains a core priority.

While we think central banks are broadly right, we have one major concern: the current regime with sticky inflation means higher rates will persist for longer, given that central banks have inflation control as their top priority. This financial picture is in stark contrast to the 15 years of ultra-low rates, quantitative easing and support provided by central banks when financial markets went into a tailspin.

Continuing the fight against inflation, while protecting growth and preserving financial stability in this new regime is not easy. There is thus a chance that central banks mis-calibrate policy and cause unintended damage, to stability, growth, or inflation. For example, in the US, not tightening sufficiently would mean that the Fed would fail to quell inflation, while tightening too much might tip the US economy into a recession. Recall how in 2011, the European Central Bank raised rates to normalise monetary conditions after the 2008 financial crisis prematurely and missed the warning signs of the European sovereign debt crisis.

The net effect: while financial markets will gradually stabilise after the shocks of the past few weeks, we should be ready for more episodes of financial stress.

Table 1: Monetary policy trajectories in select Asian economies:

2. China’s rebound has been disappointing and may continue to disappoint. Demand is recovering too slowly in the world’s second biggest economy, as consumers and businesses have been slow to regain their confidence after three years of severe pandemic controls.

Worse still, there are deeper problems: weak labour demand, a fragile property sector, and diminishing support from external demand.

In short: yes, China will recover but the rebound will fall short of expectations. In the end, the Chinese authorities will have to ramp up stimulus in order to achieve policy goals.

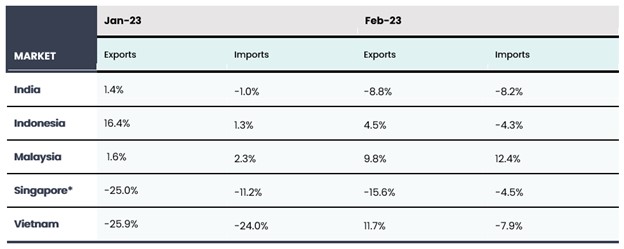

3. Select Asian economies, especially Southeast Asia, expected to do well with recoveries in tourism and foreign direct investment (FDI). While exports continue to fall, there are some signs that the worst may be soon over. The trade-reliant economies of Malaysia, Singapore and Vietnam have seen some improvement in exports performance in February 2023 – in contrast to the larger, more domestically oriented ones, such as India and Indonesia, where trade slowdowns have persisted even as domestic growth has held up. Table 2: Trade Data for Select Asian Economies (Jan-Feb 2023):

There are two bright spots for Singapore’s immediate region:

In sum, despite the uncertainty of export-driven growth, growth in FDI driven by Asia’s resilience and strong fundamentals, and a spirited recovery in regional tourism, will provide tailwinds for Southeast Asian economies.

4. Geo-political risks are contained for now. Even as the US and China trade barbs, scold each other incessantly and impose trade, tech, and other restrictions on each other, it is clear that no one wants war. The key thing is that the hard decisions on foreign and military policy are being made by leaders and officials who are rational and calculating. This is the case in the US as well as in China. This was seen in recent incidents. Tensions rose when an intelligence collecting balloon from China flew over the US. Insults were exchanged and high-level meetings were called off. But President Biden is still going to have a chat with President Xi soon and the foreign ministers of the two countries exchanged views briefly at a recent conference. The US House Speaker was persuaded to not visit Taipei – which would have inflamed Chinese tempers - but instead to meet Taiwan’s President Tsai in the US.

In the meantime, the US and China will compete in other ways. President Xi is in Moscow to strengthen China’s alliance with Russia against the US and the West. China will soon announce new initiatives to woo the Global South through a revamped Belt & Road Initiative. The US will also respond with its own initiatives.

In other words, big power contestation will go on but neither power wants to risk a war. When it comes to the crunch, sense will prevail, and it is not an accident that sense is prevailing. It is because adults are in charge in both countries.

|

This website is meant for viewing only. To place order please go to www.dollardex.com